How are listed company share buybacks considered a return of cash to shareholders?

It’s simply a company buying their own shares in the public market and adding them to their treasury stock.

What this action does do, is reduce the shares outstanding (on issue) which improves the “total shareholder return” and the “earnings per share”.

Invariably, much of senior management compensation/remuneration is based on increasing these two metrics.

By the way, buying back your own shares isn’t any stroke of genius. In fact, it’s lazy.

A company is lazy if it can’t use its excess cash for the purpose of growth such as re-investing in its own operations or acquire someone……or improve its capital/debt structure.

A dividend is the best return of cash for a shareholder but this doesn’t help the executives bonuses.

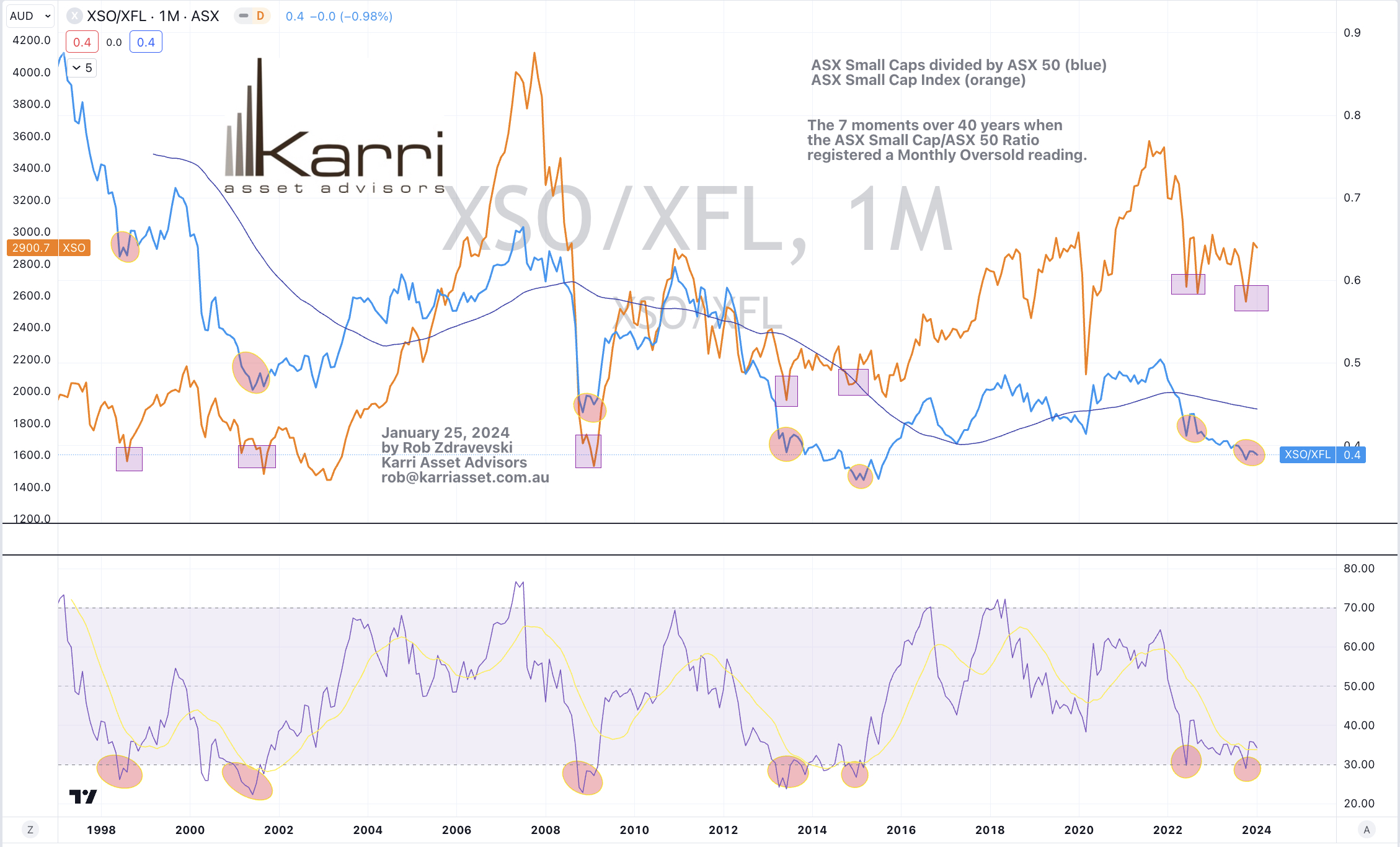

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations

Lean Hogs

Overbought (RSI > 70)

SHY

Cocoa

Rubber

Uranium

AEX

Dow Jones Industrial Average

Nasdaq 100

Nasdaq Composite

NIFTY

And the S&P 500 Index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

KLSE – the Kuala Lumper Stock Exchange

Turkiye’s BIST 100 Index

Extremes “below” the Mean (at least 2.5 standard deviations)

None

Oversold (RSI < 30)

Chile 2 year government bond yield

JKM LNG

Lithium Hydroxide

Nickel on India’s MCX Exchange

Corn

Soybean

CSI 300

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

China 10 year government bond yield

Shanghai Composite Index

Notes & Ideas:

Government bond yields were mostly lower for the week, again, even with jump in yields seen in Friday’s session.

The British 2’s, 3’s and 5’s were the exception, wth rising yields for the 2nd consecutive week).

The Japanese 2’s rose in stunning fashion. They have climbed from 0.00% to 0.10% over the past 3 weeks.

Equities were mixed, with a slight weaker bias, although many more are appearing in the overbought column.

Indonesia rose 3.5% reclaiming all of last week’s decline.

The Dow Jones Industrial Average has pout together a 4 week winning streak and has spent the past 8 weeks in overbought territory.

The S&P 500 is also in a 4 week winning streak and has risen for 13 of its past 14 weeks.

The Shanghai Composite has now registered an oversold quinella.

Amsterdam’s AEX and the Nasdaq Composite are yet to reach a new all-time high but the former did close at its highest weekly close.

The Nasdaq Transportation Index finished at its highest weekly close but yet it to break its previous all-time high. It has risen 7% in the past 3 weeks.

And Turkiye’s BIST has risen for 5 consecutive weeks making for 15% (in TRY terms) return.

Commodities were weaker with energy contracts.

To accompany that weakness in energy, WTI Crude, Brent Crude and Gasoline prices posted bearish outside reversal weeks.

Cattle is in a 5 week winning streak and has gained in 7 of the past 8 weeks. Furthermore, Cattle is still trading at extended percentages (39%) above its 200 week moving average.

Newcastle Coal broke its 7 week losing streak.

Heating Oil fell 5.5% giving up most of last week’s 6.8% rise.

Sugar is in a 5 week winning streak.

Soybeans and Corn are registering oversold extremes.

Soybeans are in a 7 week losing streak and have fallen 11 of the past 12 weeks.

JKM LNG is at its lowest close since December 20, 2020.

And Lithium Hydroxide has now spent 31 consecutive weeks in weekly oversold territory.

Amongst currencies, the AUD has seen its 5th and 6th consecutive week of declines against many pairs, which sits proportionally within my published note on December 29, 2023 that the AUD was ‘full’.

The U.S. Dollar has risen for the past 5 weeks against most pairs.

The Yen was also firmer.

The AUD/CAD, AUD/USD and AUD/INR have declined for 5 consecutive weeks. The CAD/USD has done the same.

The AUD/GBP and the AUD/SGD has fallen for 6 weeks in a row.

The EUR/GBP has eased lower for its 6th straight week.

The larger advancers over the past week comprised of;

Rotterdam Coal 5%, Cocoa 7.2%, Cotton 3.3%, JKM LNG 1.8%, Newcastle Coal 2.4%, Orange Juice 20.3%, Dutch TTF Gas 4%, Uranium 6%, Gold AUD 2.1%, Oats 2.2%, Rice 2.5%, DJ Industrials 1.4%, Indonesia 3.5%, KOSPI 5.5%, Mexico 2.4%, NIFTY 2.4%, Sensex 2%, Nasdaq Transports 2.3%, BIST 100 3.8%, ASX 200 1.9% and the ASX Small Caps rose 2.5%.

For some reference, the Nasdaq Composite and the S&P 500 rose 1.1% and 1.4% respectively.

The group of largest decliners from the week included;

Australian Coking Coal (5%), Bloomberg Commodity Index (2.1%), Baltic Dry Index (7.3%), China Coking Coal (5%), WTI Crude (7.4%), Iron Ore (5.4%), Heating Oil (5.5%), Lumber (3.4%), Lithium (12.4%), Natural Gas (4.4%), Nickel (3.4%), Platinum (2.1%), Gasoline (7.7%), S&P GSCI (3.8%), Brent Crude (6.9%), Gasoil (2.6%), Soybean (1.7%), Shanghai (6.2%), CSI 300 (4.6%), KBW Banking Index (1.7%), China A50 (4.4%), HSCEI (2.6%), Hang Seng (2.6%), KRE Regional Bank Index (7.2%), Oslo (1.7%), Helsinki (2.3%), S&P SmallCap Value (2%) and Switzerland’s fell 1.3%.

For some reference, the S&P Small Cap 600 fell 1.2%, the Russell 2000 declined 1%, the SOX closed 0.1% lower and Toronto’s TSX eased 0.2% for the week.

While I don’t care about what an athlete is paid to execute their sporting obligations, I wonder if Mercedes Benz sells less AMG (performance) vehicles and Ferrari sells more, in light of Lewis Hamilton’s decision to change employers?

Below is an image of Lewis Hamilton featuring in a #marketing campaign to sell the 2024 Mercedes GT Coupe.

Nike may have sold more golfing apparel due to Tiger Woods modelling their wares, but they may not suffer now that their mutual association has ended.

The wedding announcement and subsequent marriage is fruitful while the divorce may not have a meaningful impact.

Many people offering investment advice are very good at telling you when to ‘buy’ and not so proficient when to ‘sell’.

More importantly, how about telling you when to ‘hide’ and ‘stay away’??

‘Noise’ in the absence of research and analysis is costing investors a lot of money.

Remember the ‘buying’ hype around;

Buy Now, Pay Later companies,

Non-Fungible Tokens (NFT’s),

Neo-Banks,

Copper and electrification,

anything else involving renewable energy

and food shortages and freezing Europeans (due to the Ukraine invasion, “they” were buying Wheat, Fertilizer and Natural Gas)

16 years ago it was hype surrounding CDO/CLO (sub-prime) investment opportunities.

Today, it’s Private Credit…..

and it could be East Coast Australian real estate……

and possibly the Magnificent 7 stocks of the Nasdaq….??

Avoiding losses and carnage doesn’t show up in any of your investment performance but for others, creating the feeling that you need to participate in something new or re-invented does help the promoter or seller either make a market or a dollar.

Germany’s main stockmarket has risen about 13% over the past few months, it has climbed about 60% over the last few years and soared 580% over the past 20 years.

Over 20 years, Australia’s ASX 200 has risen 170%.

In 1999, The Economist magazine called Germany the ‘sick man of Europe’…….and every year since, some other financial media pundit or publication has done the same.

A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) either registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations

Lean Hogs

KLSE – the Kuala Lumper Stock Exchange

Nikkei 225

Overbought (RSI > 70)

Cocoa

Rubber

Uranium

Dow Jones Industrial Average

Nasdaq 100

And the S&P 500 Index

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

None

Extremes “below” the Mean (at least 2.5 standard deviations)

Shanghai Composite

Hang Seng China Enterprises Index (HSCEI)

Hang Seng (HSI)

Oversold (RSI < 30)

Chile 2 year government bond yield

China 10 year government bond yield

Nickel on India’s MCX Exchange

Lithium Hydroxide

JKM LNG

Corn

Soybean

The Oversold Quinella – Both Oversold and Traded at < 2.5 standard deviations below the weekly mean)

None

Notes & Ideas:

Government bond yields were mostly lower for the week, with the exception of the British, Japanese, Swedish and American yields.

Equities were clearly higher for the week.

The only loser of note was Indonesia on the back of upcoming general election gyrations.

The NIFTY, SOX and the CSI 300 have moved out of overbought territory

The Shanghai Composite performed an outside reversal week.

Amsterdam’s AEX is yet to reach a new all-time high.

Low and behold, Europe’s ‘sick man’, Germany closes at its all-time high while the Nasdaq has not.

And remarkably, the S&P 500 has risen 12 or the past 13 weeks.

Commodities were mostly higher.

Cattle is in a 4 week winning streak and has gained in 6 o the past 7 weeks.

Inversely, Newcastle Coal has declined for 7 consecutive weeks, while Soybeans have fallen for 6 straight weeks. The latter having fallen for 10 of the past 11 weeks.

Palladium and Corn broke their respective 4 and 6 week losing streaks.

Nickel on the LME isn’t oversold this week but remains so on India’s MCX exchange.

Lastly, JKM LNG is at its lowest close since December 20, 2020.

In last week’s edition, I alluded to Heating Oil “giving good bullish signals”. It rose 6.8% for the week.

Sugar is in a 4 week winning streak.

Gold (as priced in Australian Dollars) broke its 5 week winning streak.

Soybeans and Corn are registering oversold extremes.

Soybeans are in a 6 week losing streak and have fallen 10 of the past 11 weeks.

Cattle is still trading at extended percentages (38%) above its 200 week moving average.

And Lithium Hydroxide has now spent 30 consecutive weeks in weekly oversold territory.

Amongst currencies, the AUD has seen its 4th and 5th consecutive week of declines against many pairs, which sits proportionally within my published note on December 29, 2023 that the AUD was ‘full’.