The following assets (on a weekly timeframe) registered an Overbought reading or traded more than 2.5 standard deviations above its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

U.S. 10 year minus German 10 year bond yield spread

Natural Gas

Orange Juice

AUDUSD

CADUSD

AUDSGD

TBT

Overbought (RSI > 70)

Australian 2, 3,5 & 10 year government bond yields

Greek, Spanish, French, Italian, Portuguese, New Zealand, Swiss, French, Canadian & Korean 10 year government bond yields

German 5 and 10 year yields

U.S. 2, 5 & 10 year yields

Bloomberg Commodity & CRB Index

Uranium

Corn

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Swedish 10’s

TBX

AUDGBP

AUDJPY

Assets (securities) which touched the other side of the extreme, being Oversold (where the RSI is < 30) or were at least 2.5 standard deviations below its mean are;

Extremes “below” the Mean (at least 2.5 standard deviations)

Gold Volatility Index

Bond ETF’s TLT & IEF

Oversold (RSI < 30)

HKD/USD

Russia’s MOEX Index

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

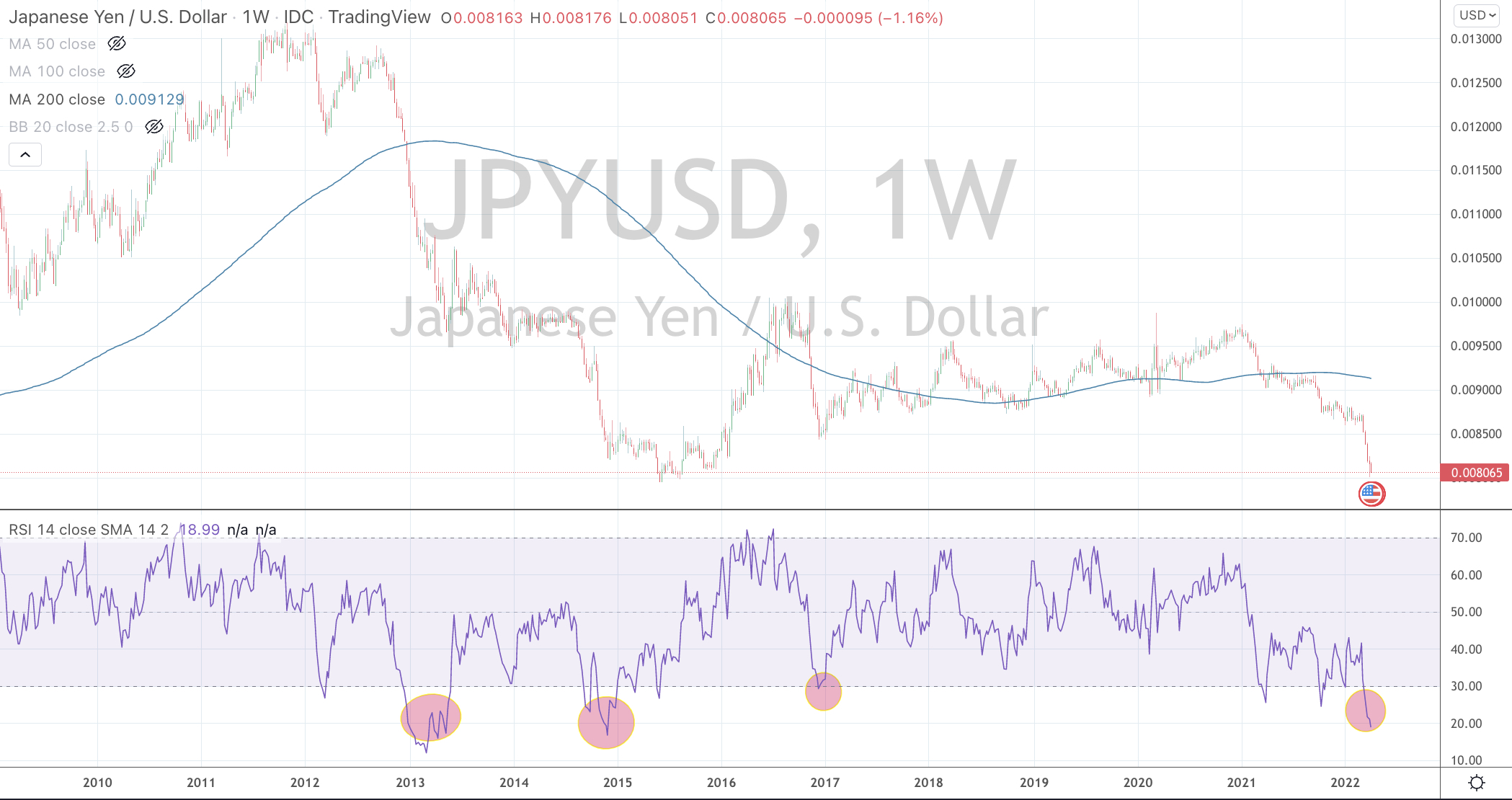

JPY/USD

U.S. 10 year minus 5 year government bond yield spread (which has now inverting and at lowest since September 2000.

Notes & Ideas:

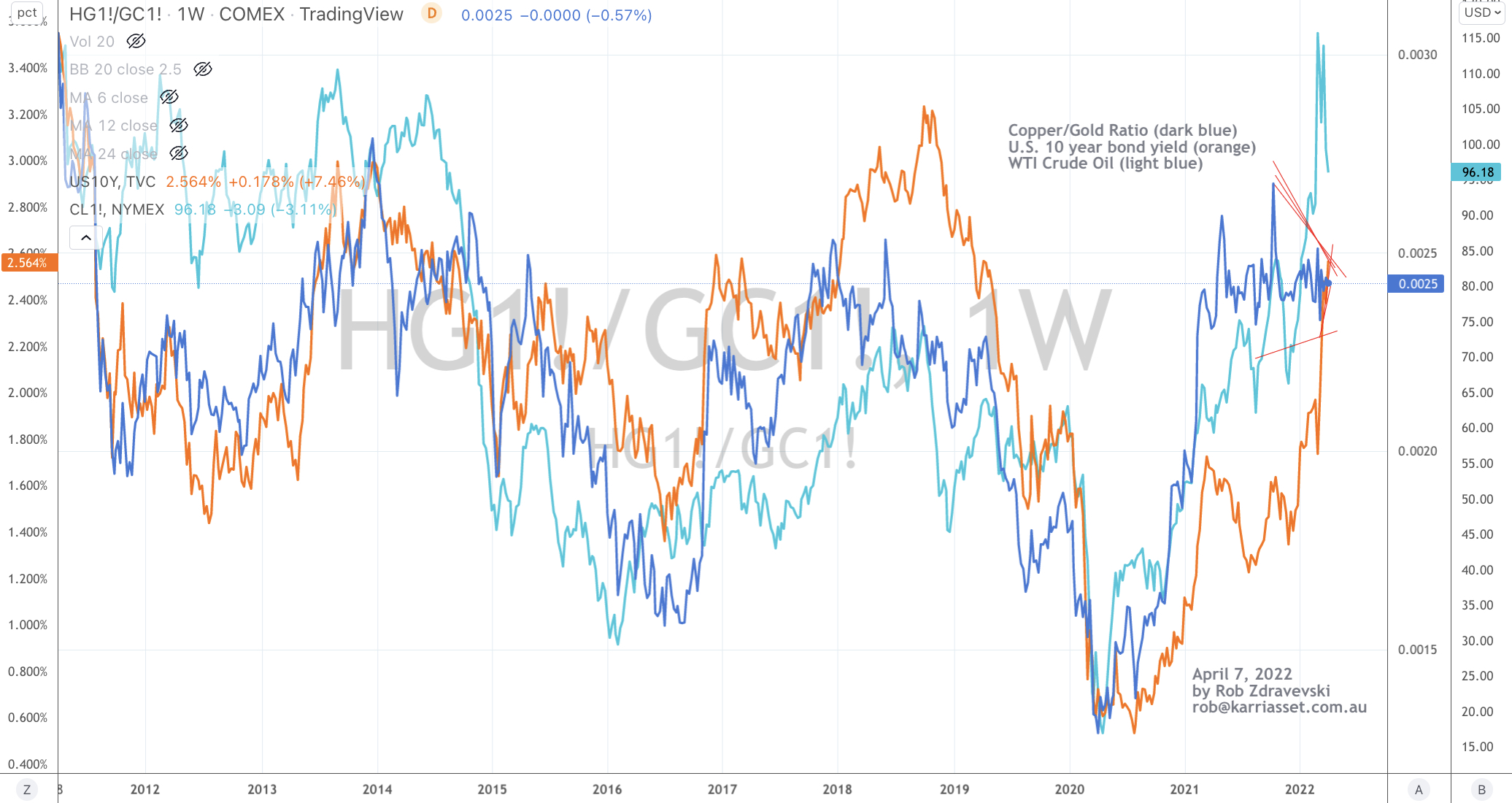

The big news for the week was in the bond market (as 10 year yields touch and tickle overbought extremes.

The U.S. yield curve inverted for a couple days and now it isn’t. Much noise (once again) for not much substance. Curves needs to invert more than a few days before probability stacks up for a future recession call.

In fact, we saw a bullish outside reversal week for the US10-02 spread and the US10-05 spread, along with the Swiss 10’s and Rotterdam delivered coal price.

The other big news is in the currency market, especially the divergence being seen in the currencies of the commodity sensitive economies of Australia and Canada.

The AUD and CAD are hitting highs against many currencies whilst the USD is also marking its own highs. These two moments seldom occur at the same time.

We’re also seeing multi-year weakness in the Yen and the Euro is getting a drubbing.

It was a mild week amongst the major global equity indices as the ASX 200 only fell 0.2% and the S&P 500 declined 1.3%, while some sub U.S. indices did see outlier weakness such as the SOX, the Russell 2000 and MidCap 400.

In expected news, the AUDEUR, the DXY and Oslo bourse are nearing overbought extremes.

Meanwhile, Bitcoin and Ethereum fell 8% for the week, meanwhile Cardano remains 67% below its September 2021 high.

Speaking of 67%, Istanbul’s BIST 100 has risen 67% since September 2021.

The larger advancers over the past week comprised of;

Rotterda, Coal 11.2%, Bloomberg Commodity Index 2%, Cocoa 2.9%, Natural Gas 9.8%, Orange Juice 6.4%, Palladium 6.7%, Sugar 5.4%, CRB Index 1.7%, Urea 2.5%, Uranium 9%, Corn 4.6%, Oats 7.4%, Soybean 6.7%, Wheat 6.8%, Swiss SMI 2.7%, FTSE 100 rose 1.8%, Istanbul surged 5.3% (up 20% in past 5 weeks) and Australia’s ASX 200 advanced 1.2%.

The group of decliners included;

Aluminium (3.6%), Australian Coal (12.6%, now down 37% in past 3 weeks), Baltic Dry Index (12.8%), China Coal (2.7%), Gasoil (6.9%), Gold Volatility Index (3.7%), Lean Hogs (2.3%), Heating Oil (3.1%), Hot Rolled Coil Steel (3.3%), JKM (3.1%), LNH (12.6%), Rubber (3.1%), Dutch TTF Gas (7.4%), Brent Crude (2%), KBW Banking Index (2.3%), CAC (2%), Dow Jones Transports (6.7%), Bovespa (2.7%), MOEX (6.1%), Nasdaq 100 fell 3.6%, Nikkei 225 (2.5%), TAIEX (1.9%), Russell 2000 (4.6%), Philadelphia Semiconductor Index “SOX” (7.3%), S&P Midcap 400 3.4%0 and S&P 500 declined 1.3%.

April 10, 2022

by Rob Zdravevski

rob@karriasset.com.au