A weekly Macro, Cross Asset review of prices trading at extremes which may generate future investment ideas and opportunities.

The following assets (on a weekly timeframe) registered an Overbought or Oversold reading and/or have traded more than 2.5 standard deviations above or below its rolling mean.

Extremes “above” the Mean (at least 2.5 standard deviations)

None

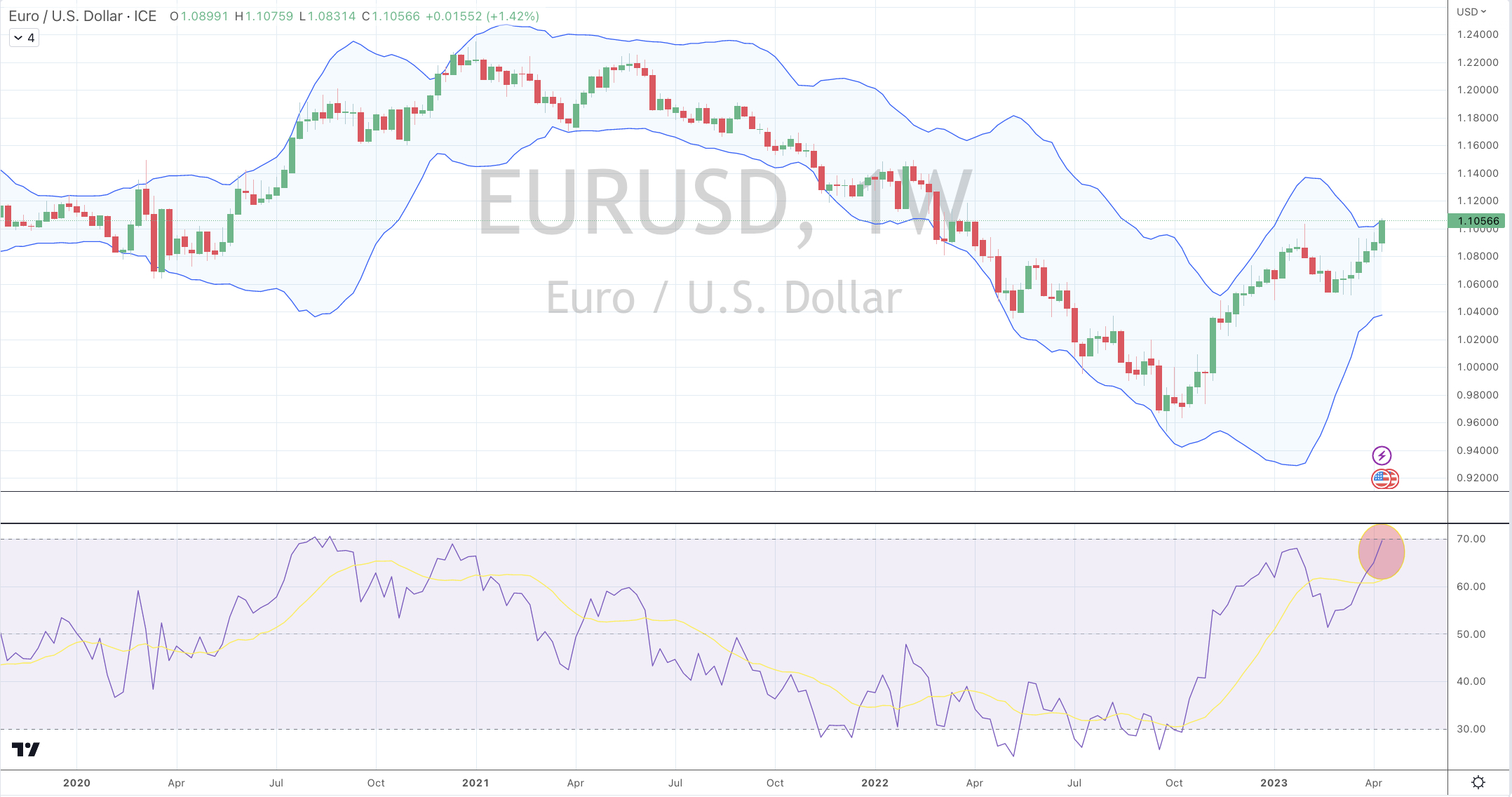

Overbought (RSI > 70)

Hot Rolled Coil Steel (HRC)

Cattle

Orange Juice

Gold (in AUD)

The Overbought Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Cocoa

Extremes “below” the Mean (at least 2.5 standard deviations)

AUD/IDR

Oversold (RSI < 30)

Urea (U.S. Gulf)

Urea (Middle East)

The Oversold Quinella – Both Overbought and Traded at > 2.5 standard deviations above the weekly mean)

Lithium

Notes & Ideas:

Equities consolidated through the week and were mostly positive for the week, with Asian bourses posting solid weekly returns.

The ASX 200 broke its 7 week losing streak

The KBW Bank Index continued to find some support.

The Nasdaq 100 continues its climb, now adding up to 11.3% over the past 3 weeks. Lagging behind is the S&P 500 having climbed ‘only’ 6.4% over the same time.

Heck, Stockholm’s OMX 30 did 6.5% just this week alone.

Ahh, remember when that was considered an adequate return for the year?

Amongst bonds, yields generally rose across the government debt of the world.

Many of the spreads listed as ‘extremes’ in last week’s edition are no trading there now. The same is for other bond yields.

Commodities were generally stronger with strength saw support across the energy complex except for the Gases.

Strength in Crude Oil also helped the commodity indices get out of Oversold territory. In fact, WTI Crude has risen 12.7% in 2 weeks.

It’s worthy to note that U.S. Mid West Hot Rolled Coil (HRC) Steel has doubled over the last few months,

And Gold in CAD is no longer Overbought.

In currencies, the AUD was steady to firm amongst its crosses whilst the Yen saw weakness against everyone.

The larger advancers over the past week comprised of;

Aluminium 3.3%, Rotterdam Coal 4.3%, Bloomberg Commodity Index 2.4%, Cocoa 1.7%, WTI Crude 9.3%, HRC Steel 10.1%, JKM LNG 6.4%, Cattle 3.3%, Tin 10.9%, Nickel2.7%, Orange Juice 6.1%, Palladium 3.8%, Platinum 2%, Gasoline 3.6%, Sugar 6.9%, SPGSCI 4.5%, CRB Index 3.6%, Cotton 8.2%, Dutch TTF Gas 16.4%, Brent Crude 7%, Silver in AUD 3.1%, Silver 3.9%, Corn 2.7%, Soybean 5.4%, AEX 3.3%, KBW Banks 4.7%, CAC 4.4%, DAX 4.5%, DJ Industrials 3.2%, DJ Transport 5.3%, MIB 4.7%, HSCEI 2.6%, Hang Seng 2.4%, IBEX 5%, Bovespa 3.1%, Nasdaq Composite 3.4%, KOSPI 2.6%, S&P MidCap 400 4.6%, Nasdaq Biotech 2.4%, Nasdaq 100 3.3%, Nikkei 225 2.4%, Oslo 4.5%, Copenhagen 3.2%, Helsinki 3.6%, Stockholm 6.5%, Russell 2000 3.7%, Sensex 2.6%, S&P SmallCap 600 3.9%, Swiss SMI 4.4%, SOX 3.5%, TSX 3.1%, FTSE 100 3.1% and Australia’s ASX 200 rose3.2% and the ASX Small Caps climbed 4.3%.

The group of decliners included;

Australian Coking Coal (14.6%), Baltic Dry Index (6.7%), China Coal (7.1%). Lean Hogs (2.5%), Heating Oil (2.8%), Coffee (4.9%), Lumber (10.2%), Urea Middle East (5.8%), Gold in CAD (2.1%) and Rice fell 2.6%.

April 2, 2023

by Rob Zdravevski

rob@karriasset.com.au