Is risk at a stretch?

February 1, 2021 Leave a comment

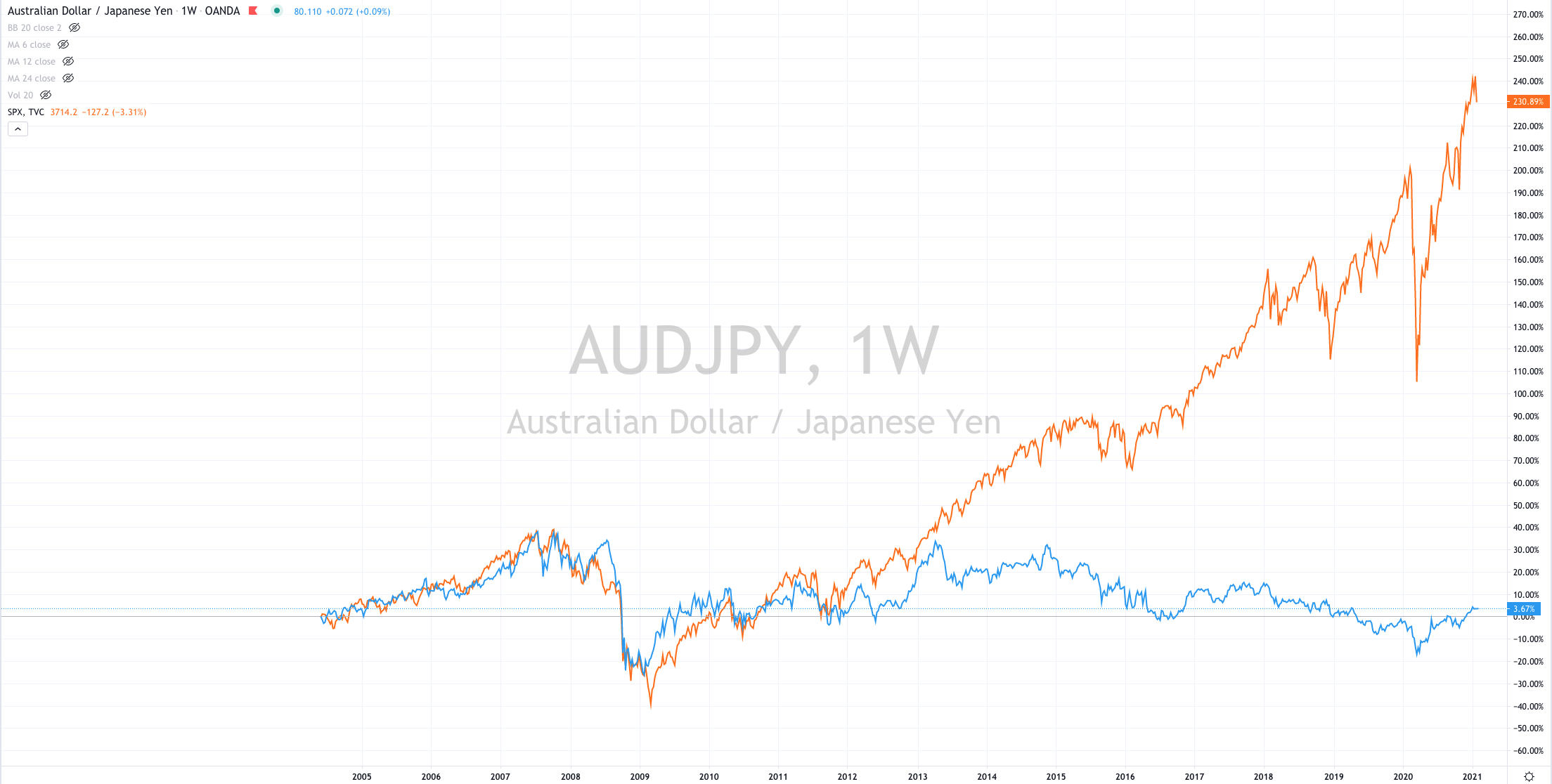

The SPX vs AUDJPY spread – Part 1

Here is a story when the S&P 500 changed its risk profile.

Half way through 2013, the S&P 500 decided it would no longer honour, let alone couple with its old ‘risk’ companion…..the AUD/JPY currency cross.

So what gives?

Does the S&P 500 need to fall sharply in order to ‘re-couple’ ?

Well, there isn’t any rule which suggests so.

I’m merely pointing out an extreme.

Equally, it seems unlikely the AUD would strengthen against the Yen, for if equities declined notably, the safe-haven Yen would be bought and the risk ‘associated’ AUD would be sold.

So, there goes your spread trade theory.

Let the dance continue for now, but the multi-year bet is for equity risk premia to converge.

More on the near-term picture in a moment.

February 1, 2021

by Rob Zdravevski

rob@karriasset.com.au