the study below updates the most recent percentage figure that the SENSEX is trading above its 200 week moving average.

While Indian equity markets have resembled an ‘investible’ market over the past decade, there are times when to tune into the peaks and troughs when deploying capital there.

It seems to be a dance between mean reversion and mean convergence.

Anecdotally, folks are expressing interest in Indian equities.

Inversely, the Chinese equity market hasn’t resembled anything close to being investible for more than 15 years.

While not registering overbought signals, the SENSEX Index in India is currently trading at a higher level within its range, prompting the need for a thorough examination of the probabilities involved of further advance.

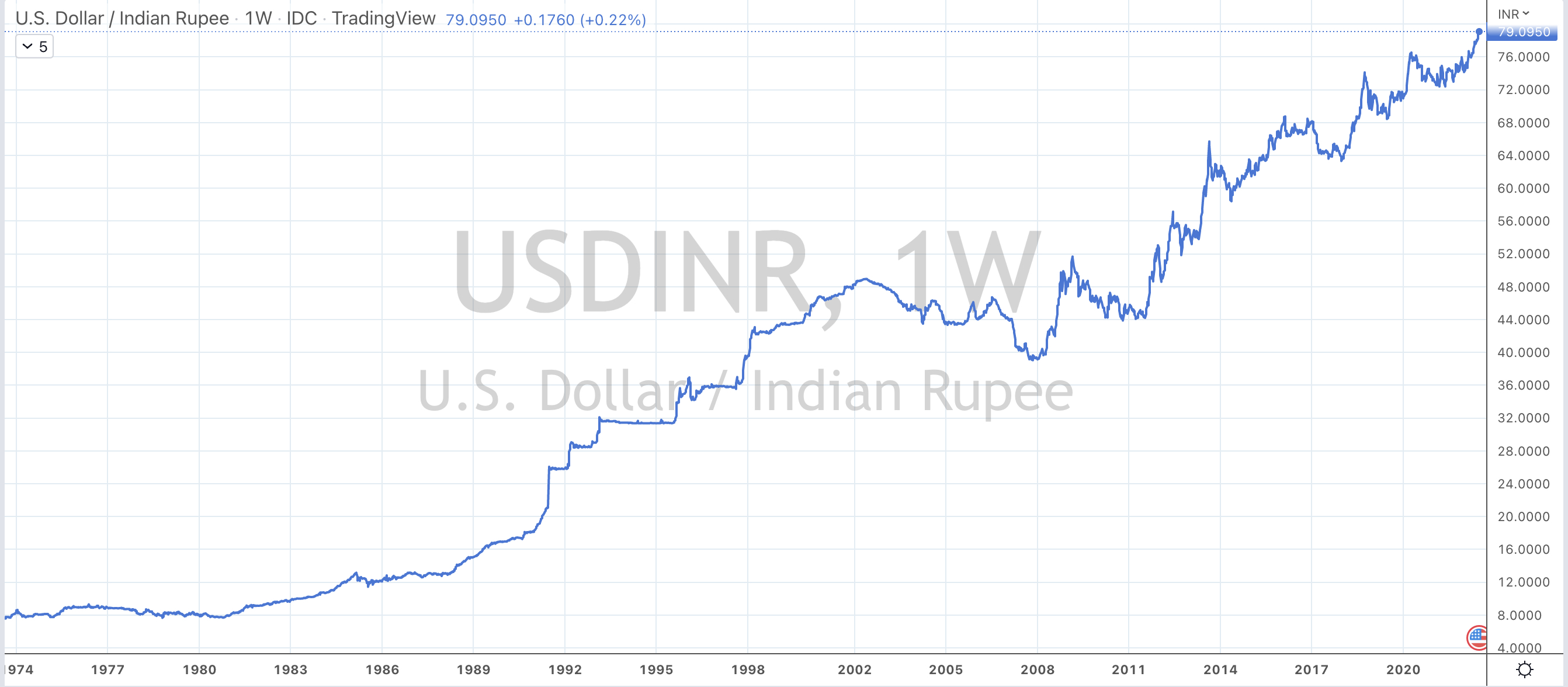

The Indian Rupee has lost 25% of its value against the U.S. Dollar over the past 3 years.

While Indian assets may be considered to be ‘on sale’ in U.S. Dollar terms, the 50 years of continued weakness in the Indian Rupee certainly makes Indian exports (including services) much more competitive……

It does hurt the country when needing to pay for goods in USD, Euro or in Russian Rubles when it comes to buying oil.

The upside is that it does provide ‘bang for one’s buck’ when remitting monies back to India especially when its U.S. Dollars.

In fact, annual foreign remittances into India accounts for at least 3% of annual GDP being approximately $87 billion worth.

However, the stronger U.S. Dollar (and inversely the weaker Rupee) also tempts more Indian talent and labour to leave its shores as they chase higher earning and purchasing power.

Unfortunately, I don’t have any view or suggestions how to change this trend.